Why DSCR breaches are increasing, and what credit teams should watch

Higher rates, tighter margins, slowing growth. The textbook combination for a covenant breach wave. Here's what the leading indicators actually look like.

CovenantFlow Team

Catalyze Labs

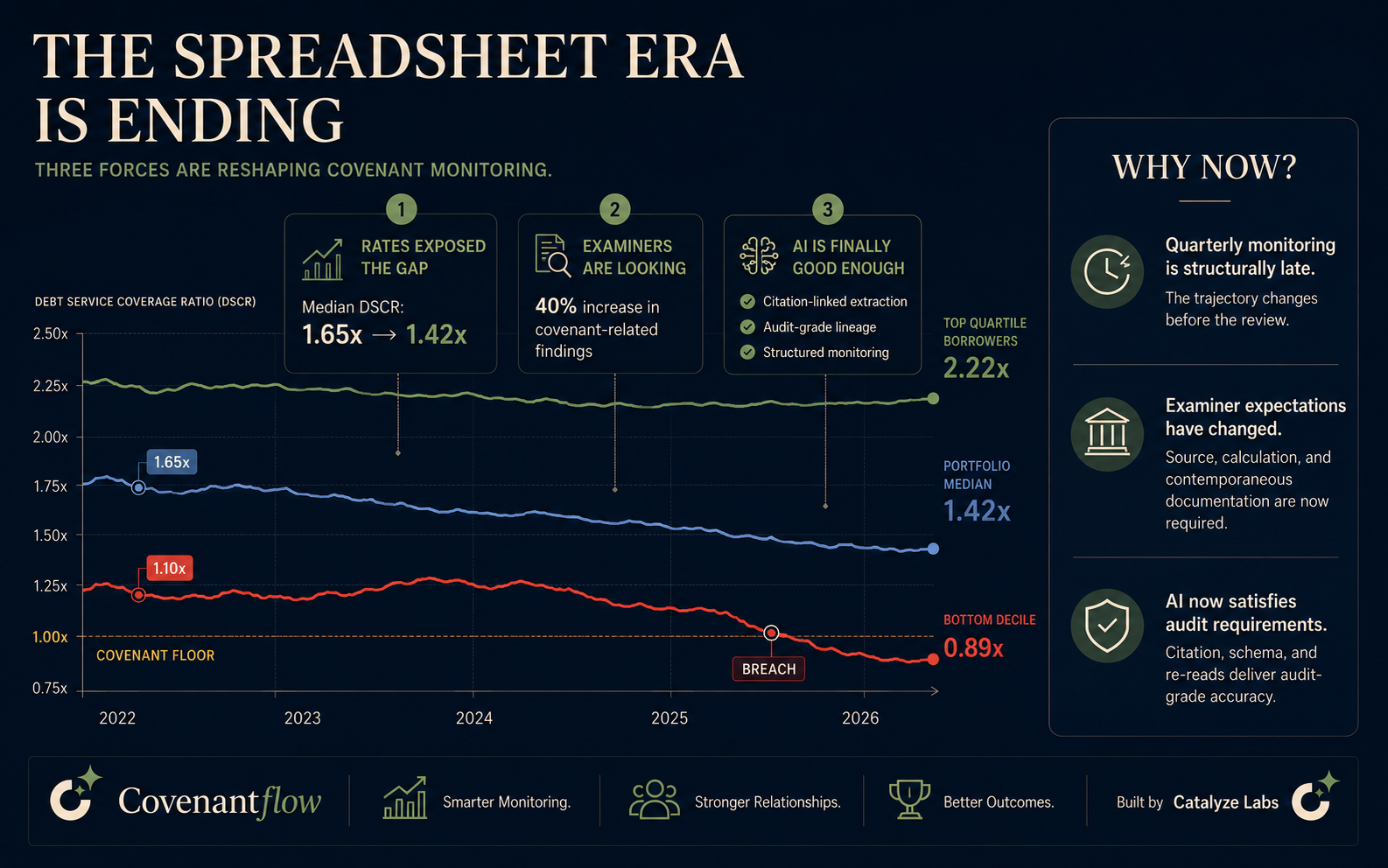

Across the commercial books we monitor, the median DSCR has moved from 1.65x in early 2024 to 1.42x today. That is not a panic-level shift on its own, but the tail matters: the bottom 10% of borrowers used to sit around 1.20x, right at the typical covenant floor, and now that decile sits at 1.08x.

Three factors are driving this.

The first is the obvious one: rates. Debt service has gone up faster than operating income. Most loans booked between 2020 and 2022 carried fixed rates well below where new originations price today; refinances or maturity extensions land at 200+ bps higher.

The second is margin compression. Wage growth, healthcare costs, and SaaS spend have eroded operating margins for borrowers in services and retail. Manufacturing has been more resilient, but only because input prices stabilized last year.

The third is slower revenue. Many mid-market commercial borrowers see softer Q1 numbers than their Q1 2025 projections.

For credit teams, the practical implication is to pull DSCR forward as the leading indicator. A covenant breach is a lagging metric. By the time it triggers, the trajectory has been deteriorating for 2 to 3 quarters. Tracking DSCR drift quarter over quarter, with alerts at, say, 0.10x movement against threshold, surfaces the problem before it becomes a problem.